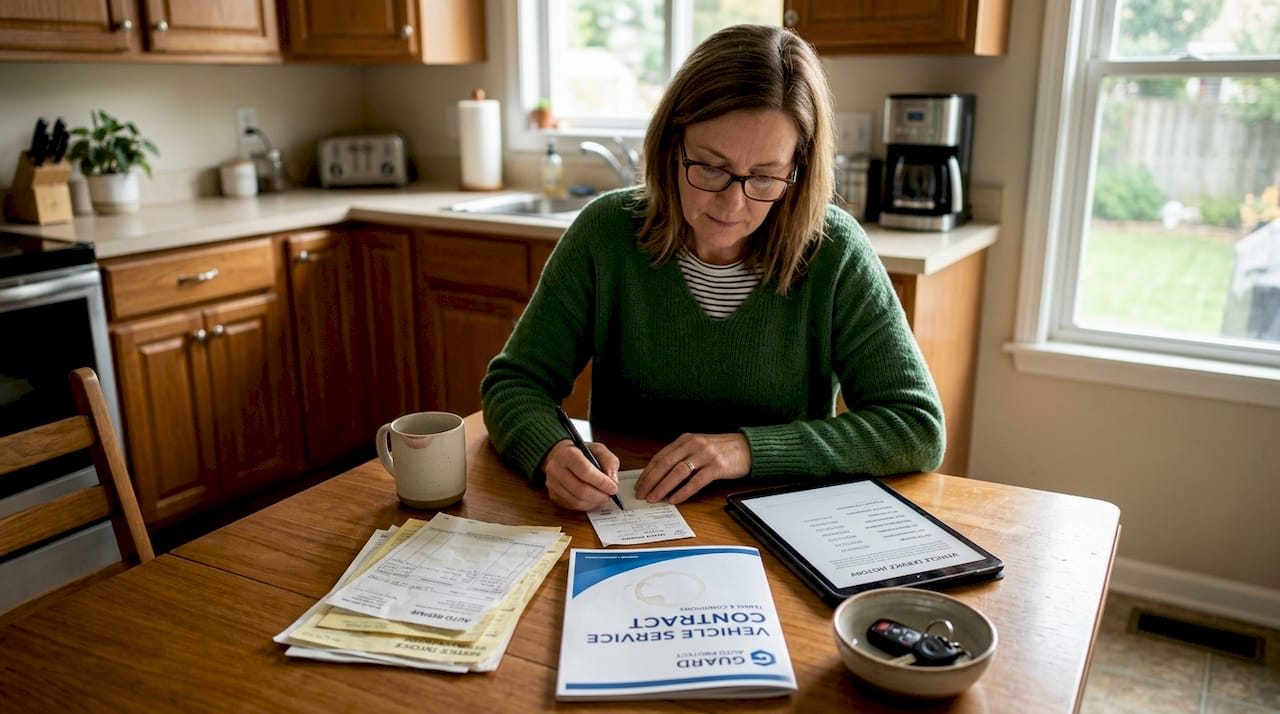

When a major repair bill lands on your doorstep after your factory warranty expires, the shock can be real. The average approved claim payout on a vehicle service contract is $4,127, which tells you exactly how expensive modern car repairs have become. Many owners assume their coverage just "rolls over" somehow, only to discover there's a gap between what the manufacturer covers and what comes next. A vehicle service contract (VSC) is one tool designed to bridge that gap, but it works very differently from a standard warranty. This guide breaks down what a VSC is, how it works, what it costs, and whether it makes sense for your situation.

Table of Contents

- What is a vehicle service contract?

- Types of coverage and key exclusions

- What does a vehicle service contract cost and pay out?

- Pros, cons, and how to choose a provider

- The overlooked truth about vehicle service contracts

- Discover top vehicle service contract options

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Not the same as warranty | A vehicle service contract is a separate, optional contract that covers specific repairs after your factory warranty ends. |

| Coverage and exclusions vary | Not all parts or systems are covered, so always review exclusions and required documentation before purchasing. |

| Know the risks and benefits | VSCs offer peace of mind but come with costs, claim denial risks, and the need to pick reputable providers. |

| Best for certain owners | Owners of high-mileage or older cars, or those unable to handle major surprise repairs, benefit most from VSCs. |

What is a vehicle service contract?

A vehicle service contract is not a warranty, even though dealers and sellers often use those words interchangeably. The Federal Trade Commission is clear: a VSC is an optional agreement, separate from the manufacturer warranty, that pays for certain repairs after the warranty expires. That distinction matters because it affects your legal rights, who you deal with when something goes wrong, and what protections apply.

VSCs are sold by three main groups: automakers (through their dealership networks), independent dealerships, and third-party companies. Each seller operates under different rules and offers different contract terms. Automakers tend to offer more standardized plans, while third-party providers can vary widely in reliability and coverage quality.

Here's what makes VSCs confusing for most buyers. A factory warranty is included in the purchase price of a new car and is backed directly by the manufacturer. A VSC is a separate purchase, often offered at the point of sale or through direct mail campaigns, and it is backed by whoever sold it to you, not necessarily the automaker. Understanding the difference between warranties and service contracts helps you ask the right questions before signing anything.

A VSC typically covers specific mechanical or electrical repairs listed in the contract. Common covered items include:

- Engine components

- Transmission and drivetrain parts

- Electrical systems

- Air conditioning and heating

- Steering and suspension (depending on plan level)

- Roadside assistance (often bundled)

"A vehicle service contract is an optional agreement, separate from the manufacturer warranty, that pays for certain repairs after the factory warranty expires." — Federal Trade Commission

The key phrase there is "certain repairs." A VSC is not a blank check for any problem your car develops. Coverage is defined precisely by the contract language, and what is not listed is generally not covered. That is why reading every page before you sign is non-negotiable.

Types of coverage and key exclusions

Now that you know what a vehicle service contract is, it's crucial to understand the levels of coverage and exactly what's not included. The California Department of Insurance outlines three main tiers that most contracts fall into, each with different price points and deductible structures.

| Coverage level | What it covers | Best for |

|---|---|---|

| Powertrain | Engine, transmission, drive axles | Budget-conscious buyers, older vehicles |

| Powertrain Plus | Powertrain plus electrical, A/C, steering | Mid-range protection needs |

| Exclusionary (bumper-to-bumper) | Everything except listed exclusions | Newer vehicles, maximum protection |

Exclusionary plans are the broadest and most expensive. Instead of listing what is covered, they list what is not covered. That approach gives you more protection by default, but it still comes with real limits.

The FTC notes that common exclusions across nearly all VSC contracts include:

- Normal wear and tear (brake pads, belts, tires)

- Routine maintenance (oil changes, filters, fluid flushes)

- Damage from accidents, floods, or fire

- Pre-existing conditions at the time of purchase

- Modifications or aftermarket parts

- Cosmetic damage (paint, upholstery, trim)

- Rust or corrosion

Most contracts also require repairs to be done at an approved facility. Using an unauthorized shop, even a trusted local mechanic, can void your claim entirely.

Contracts also come with specific term limits. Most are structured around a combination of years and mileage, such as 3 years or 36,000 miles, whichever comes first. Deductibles typically range from $0 to $200 per repair visit, and some contracts use a "per-visit" deductible while others apply it "per-repair-item," which can significantly change your out-of-pocket cost.

Pro Tip: Before you buy, ask the seller for a sample contract and flip straight to the exclusions section. If the seller resists or says the exclusions are minimal, that is a red flag. Legitimate providers will give you the full document before you commit.

Also keep your maintenance records organized. Many VSC providers require proof that you followed the manufacturer's recommended service schedule. Missing an oil change record can give a provider grounds to deny a claim, even for an unrelated repair.

For a side-by-side look at top vehicle warranty companies and what each plan level typically includes, comparing multiple providers is a smart first step.

What does a vehicle service contract cost and pay out?

Knowing what is covered is only part of the story. Cost and claims statistics play a huge role in the real value of a vehicle service contract.

VSC pricing varies based on your vehicle's age, mileage, make, and the coverage level you choose. Entry-level powertrain plans can start around $1,000, while exclusionary coverage on a high-mileage luxury vehicle can exceed $4,000 or more. Most plans allow monthly payment options, which makes the upfront cost easier to manage.

Here is where the numbers get interesting:

| Metric | Statistic |

|---|---|

| Average approved claim payout | $4,127 |

| Claim denial rate | 22.4% |

| New car buyers who purchase a VSC | 24% |

| Claims related to powertrain repairs | 68% |

These figures come from industry-wide VSC data and paint a clear picture. The average payout is substantial, which means a single covered repair can justify the cost of the contract. But the 22.4% denial rate is also worth taking seriously. Nearly one in four claims is rejected, often due to documentation gaps, excluded parts, or the repair being performed outside the approved network.

The fact that 68% of claims involve powertrain repairs reinforces why powertrain coverage is the most popular entry point. Engines and transmissions are the most expensive components to fix, and they are also the most likely to fail on older or high-mileage vehicles.

Pro Tip: Keep a dedicated folder, physical or digital, with every oil change receipt, tire rotation record, and scheduled maintenance invoice. If you ever file a claim, that paper trail can be the difference between approval and denial.

If you want to see what coverage actually costs for your specific vehicle, you can compare VSC quotes side by side, or get a free VSC quote to start with a baseline number.

Pros, cons, and how to choose a provider

Understanding costs and payouts sets the stage for a balanced look at both the advantages and potential pitfalls of VSCs.

The real advantages:

- Protection against large, unexpected repair bills

- Predictable monthly costs instead of surprise expenses

- Peace of mind, especially for high-mileage vehicles

- Transferability to a new owner, which can increase resale value

- Roadside assistance and rental car coverage often bundled in

- Useful for people on fixed incomes or tight budgets who cannot absorb a $3,000 to $5,000 repair bill

The real drawbacks:

- Can be expensive relative to the repairs you actually need

- May overlap with remaining factory warranty coverage

- Claim denial rates mean not every repair gets paid

- Some providers are unreliable or operate deceptively

- Monthly payments add up if you rarely file claims

The FTC advises consumers that VSCs can protect against large repair bills and offer peace of mind, but they can also be expensive, overlap with existing warranties, and are sometimes marketed through deceptive practices.

"Be wary of unsolicited calls or mailers. Legitimate VSC sellers do not need to pressure you into a same-day decision."

Here is a step-by-step approach to choosing a trustworthy provider:

- Verify the provider is licensed in your state

- Request a full sample contract before any payment

- Compare at least three providers on coverage terms, not just price

- Check reviews on the Better Business Bureau and Trustpilot

- Confirm which repair shops are in the approved network

- Ask about the cancellation policy and refund terms

- Never sign under high-pressure sales tactics

To find vetted, state-licensed options, you can find reputable providers filtered by your location and vehicle type.

The overlooked truth about vehicle service contracts

Most car owners who regret buying a VSC share one thing in common: they focused on the sales pitch and skipped the fine print. They assumed "bumper-to-bumper" meant everything was covered. It does not. Every contract has exclusions, and those exclusions are written to protect the provider, not you.

Here is something most articles will not tell you. The risk of provider failure is real. Some VSC companies have gone out of business mid-contract, leaving customers with no coverage and no refund. That is why checking a provider's financial backing and state licensing matters as much as the coverage terms themselves.

States typically require a 30-day cancellation window, and some mandate full refunds within that period. Use that window. Buy the contract, read every clause at home without pressure, and cancel if anything does not add up.

VSCs make the most sense for owners keeping older or high-mileage vehicles, or anyone who genuinely cannot absorb a surprise $4,000 repair. For someone with a late-model car still under factory coverage, the math rarely works in their favor. Understanding the full warranty contract details before you commit is the single most important step you can take.

Discover top vehicle service contract options

Vehicle service contracts vary more than most people realize, from what they cover to how claims are handled and who stands behind the contract. Navigating those differences on your own takes time, and the wrong choice can cost you more than no contract at all.

Our platform makes it easier. We've reviewed and rated top vehicle warranty companies based on coverage quality, customer satisfaction, and claims handling. If you're still building your knowledge base, our auto warranty basics section is a great starting point. Ready to compare real options? Browse best providers in your state and find a plan that fits your vehicle and your budget.

Frequently asked questions

Is a vehicle service contract the same as an extended warranty?

No. A vehicle service contract is a separate, optional contract that covers certain repairs after the factory warranty ends, while an extended warranty is technically an extension of the original manufacturer warranty.

What repairs are usually covered by a vehicle service contract?

Most VSCs cover major mechanical components like the engine and transmission, but coverage depends on the plan level. Exclusionary plans cover the most, while powertrain-only plans are the most limited.

What are the most common reasons for VSC claim denials?

Claims are most often denied due to missing maintenance records, repairs performed at unauthorized shops, or pre-existing conditions and exclusions that were listed in the contract but overlooked at purchase.

Who should consider buying a vehicle service contract?

VSCs are best suited for owners of older or high-mileage vehicles, or anyone who cannot afford major out-of-pocket repairs in the $3,000 to $5,000 range without serious financial strain.

How do I avoid scams when shopping for a vehicle service contract?

Buy only from state-licensed providers, avoid deceptive phone or mail offers, and always read the full contract before signing anything or making any payment.